As this article is a must-read in my opinion, but is printed in Dutch, here follows an integral translation of it:

Germany already sponges on foreign demand for a long, long time; just like China (by Marcel de Boer).

Analists like to use big words. When it concerns the economic growth in Germany Germany Germany Germany pull the rest of Europe up to a higher growth level’. For this reason the IMF advises Germany

Especially from the consumer’s side there is hardly an impulse for growth, at least not through his spendings. Retail sales is hardly moving upwards. To state it stronger: over the last months there has been a decrease in retail sales.

The restraint of the German Joe the Plummer, here called “Otto Normalverbraucher” (Otto Average-User) is not a new phenomena. He sits on his cash for years, already. That is no mystery; from the economic growth, he sees hardly anything back on his pay slip. An investigation executed by the economic institute DIW from Berlin, of which the results were published last week, showed that Germany employees LOST 2.5% in real income over the last ten years. The hardest hits were suffered at the bottom of the salary scales: some employees lost over 22% of real income.

German households were convinced to accept a smaller and smaller slice of the economic growth- pie, according to Michael Pettis of think tank Carnegie Endowment. For more than a decade these households subsidized German economic growth, with far-reaching consequences for the rest of Europe .

Around the new millennium, Germany chose a path of wage restraint, just like The Netherlands Portugal and Spain

Under the lead of the social-democrat German chancellor Gerhard Schröder, the consumer was made subordinate to the German trade and industry. Quickly, consumption lagged with production, according to Pettis. The surplus in goods and services was sold abroad, almost exclusively in Europe and especially in the part now called “the peripheral countries”: Portugal , Spain , Italy and Greece

Normally, it doesn’t take long before a country with a trade surplus sees its currency increase in value. However, as the Euro was deployed, this was not possible. Within the Euro-zone, Germany had an undervalued currency, while the countries that imported Germany

Implicitely, this was like a tax charge on German imports, according to Pettis. A charge, that acted like a subsidy for the German industry. In the peripheral countries, the industry was ‘taxed’ to subsidize imports. In a short matter of time, Germany could turn its lagging competitiveness into a lead: in 2000 Germany

As a consequence of the common currency, a situation evolved within the Euro-zone that could be compared with the relation between the US and Greece : as a consequence of underconsumption in China , together with the coupling of the yuan to the dollar, overconsumption evolved in the US

But the equasion goes further. China Germany (just like The Netherlands

Against these surplusses, there are equally large deficits on the capital account. Eventually, the external account must be balanced. An outflow of money from Germany

The peripherals should have used the cheap money to reinforce the structure of their economies. They received this advice from the ECB month after month, but ignored it. The money was mainly used for consumption and when it was invested, it was spent in the housing market, that was blown up to a bubble of massive proportions.

After five years, Germany China and Japan

But eventually the system stalls, as becomes clear in peripheral Europe and the United States Greece , Europe chooses for the last two possibilities. At the same time, people are aiming at an internal devaluation in the whole periphery. Through a decrease in wages and prices, the countries should become competitive again. However, when the Northern surplus countries are not willing to increase their consumption to a level above their production level, an deflatory hole originates and it will take a long time before European growth will be started again.

I was already aware of the dangers of the current imbalances within Europe , but this article explained it all in a wonderful, concise way.

And I’m convinced that Marcel de Boer is totally right in his conclusions on the German economy.

However, it will not be easy to increase consumption in Germany

I don’t want to advocate for enabling a price-wage spiral in Germany

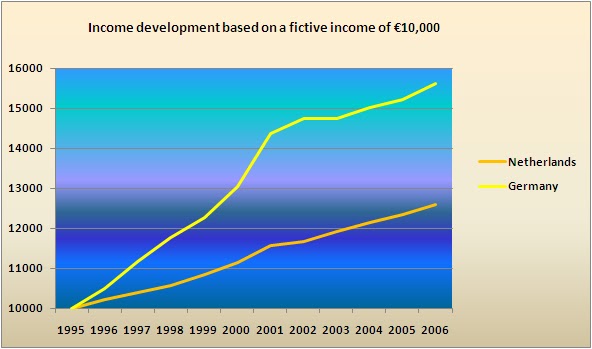

Although I don’t have the correct figures on the net income of German households, I’ve gathered some Eurostat statistics (ec.eurostat.eu) on the income development of German households, compared to Dutch households and put them in two graphs: the first graph shows the income development as a percentage of growth from 1996-2006 and the second graph shows the consequences of this income growth, based on a fictive annual salary of €10,000. I took Dutch data in comparison, as both countries are large net exporters and the people have a lot in common. Unfortunately, I don’t have more recent and detailed data available, but I think these graphs are still very telling:

|

| Income development as a percentage of growth in The Netherlands and Germany 1996-2006 source: ec.eurostat.eu |

|

| Income development in The Netherlands and Germany from 1996-2006, based on a fictive income of €10,000 (source: ec.eurostat.eu) |

These graphs show clearly the influence of a prolongued period of reduced income growth (Germany) on the spendable income, compared to a situation of ‘normal’, tendency-sensitive growth (The Netherlands). Based on a fictive start income of €10,000, reduced income growth resulted already in a difference in income of €3000 between Germany and The Netherlands. As the real incomes were probably higher, the difference will also be much bigger. This explains why the average German can’t spend so much, even if he had a desire to spend. This is especially true at the lower incomes, where the hardest hits were suffered.

Although the spending situation for consumers in The Netherlands in average is about the same as in Germany, the cause is different: the income growth, combined with the extremely low interest rates of the last 15 years, led to a spending spree in housing. Where a house in 1995 costed €100,000, the average price in 2007 was about 2.7 times higher: €270,000. This caused an extreme lock-up of money in housing and as a consequence reduced spending on (durable) consumption goods.

As a consequence of the locked-up Dutch housing market during the last four years and therefore the unability of Dutch houseowners to decrease their spendings on housing, the Dutch consumer is still very cautious about spending his income on consumption and durable goods. This effect is reinforced by the quite negative social mood and the credit crisis that resulted from this social mood.

Whatever the cause may be, the effect is that the cumulative imbalances between the northern and the southern European countries will not be balanced out, until consumption in The Netherlands, Germany and the other surplus countries is higher than production for a number of years. And that is bad news for whoever thought that the problems with the PIIGS-countries are over, since the last rescue attempt for Greece.

No comments:

Post a Comment