The Dutch housing situation is akin to

a bubble again, almost purely based upon speculation and expat housing in the

big cities. It might explode sooner than

you think, as the underlying wage growth is actually negative.

Everybody

who would take a look at the Dutch housing market in 2018, would think that the

Dutch economy is growing dramatically at the moment.

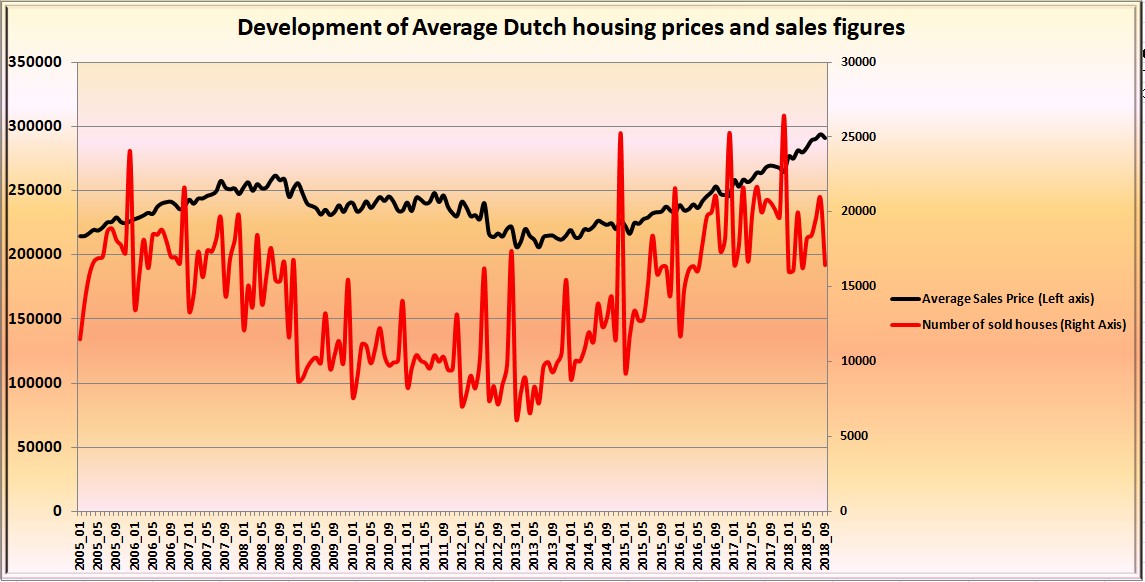

Since

June, 2013 – identified as the trough in

the average Dutch housing prices since the housing crisis started in 2007(!) – the

average house price rose by a staggering 41%, to €291.000 from €206.000. These

figures are based upon data from Statline, the online database of the Dutch Central Bureau of

Statistics.

And

while these data are slightly distorted by the sturdy price growth in large

cities like especially Amsterdam and Utrecht, the general feeling in the rest

of the world could be that the sky is the limit again in The Netherlands.

|

The average housing prices and the average sales numbers

in The Netherlands from 2008 - 2018

Chart by: Ernst's Economy for You

Data courtesy of statline.cbs.nl

Click to enlarge |

The

uninformed reader could think – based upon these shiny figures of the Dutch

housing market – that the Dutch average wages have grown dramatically since

2013. Yet, that is not the case, as the following chart shows:

|

The average collective wage rise vs inflation

in The Netherlands from 2010 - 2018

Chart by: Ernst's Economy for You

Data courtesy of statline.cbs.nl

Click to enlarge |

To

the contrary, I would say. As a matter of fact the collective labour agreement wages

(i.e. CAO wages), as negotiated by the labour unions, have not grown at all in

comparison with the inflation. The black line in the second chart represents

the net effective wage growth in The Netherlands, when corrected for inflation.

The

grim conclusion for The Netherlands is that there was actually a net wage

decrease for the middle and lower income groups, who are mostly bound by the

CAO wages. This wage decrease is caused by the rise in consumer prices for all

kinds of goods and services, as well as the sturdy growth in local and central

taxes and levies.

Then

the multi billion euro question is: what did cause this extraordinary growth in

housing prices in The Netherlands in a time when wages did not grow at all?

My

answer is: probably the causes are pure speculation – based upon financing

against the still near-zero interest rates that large investors have to pay – at one hand and the soaring demand for housing

on behalf of expats and foreign knowledge workers in the urban areas at the

other hand.

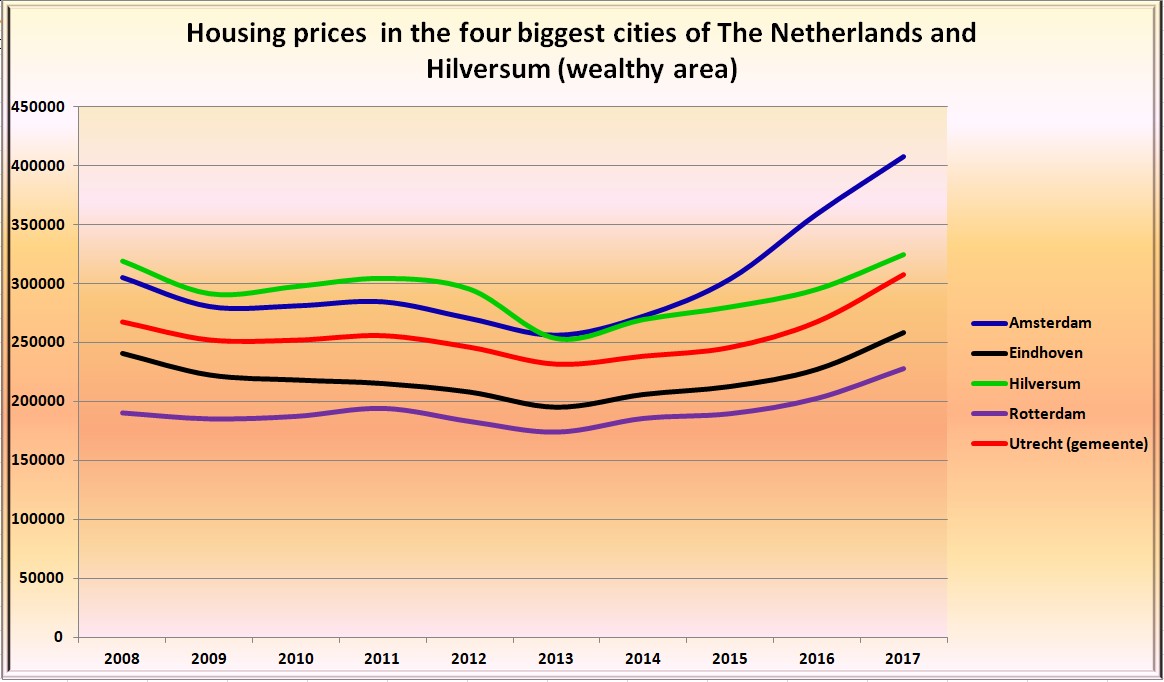

|

The average housing prices in the largest cities and

wealthy areas from 2010 - 2018

Chart by: Ernst's Economy for You

Data courtesy of statline.cbs.nl

Click to enlarge |

Especially

Amsterdam and Utrecht as well as the cities closeby are very popular among expats

and knowledge workers from around the globe, as the aforementioned chart shows.

Amsterdam “enjoyed” a 60% raise in housing prices since 2013 and also Utrecht

saw a 33% growth since the same year.

The

companies and institutions who hire these expats and knowledge workers are mostly

more than willing to pay topdollar for a small house or condo at close range,

as it is still a relatively low expense in comparison with the labour costs of

these workers themselves. This circumstance probably fueled the broad

speculation by all kinds of private and corporate landlords in Amsterdam and

Utrecht and makes that the housing prices have soared in those areas.

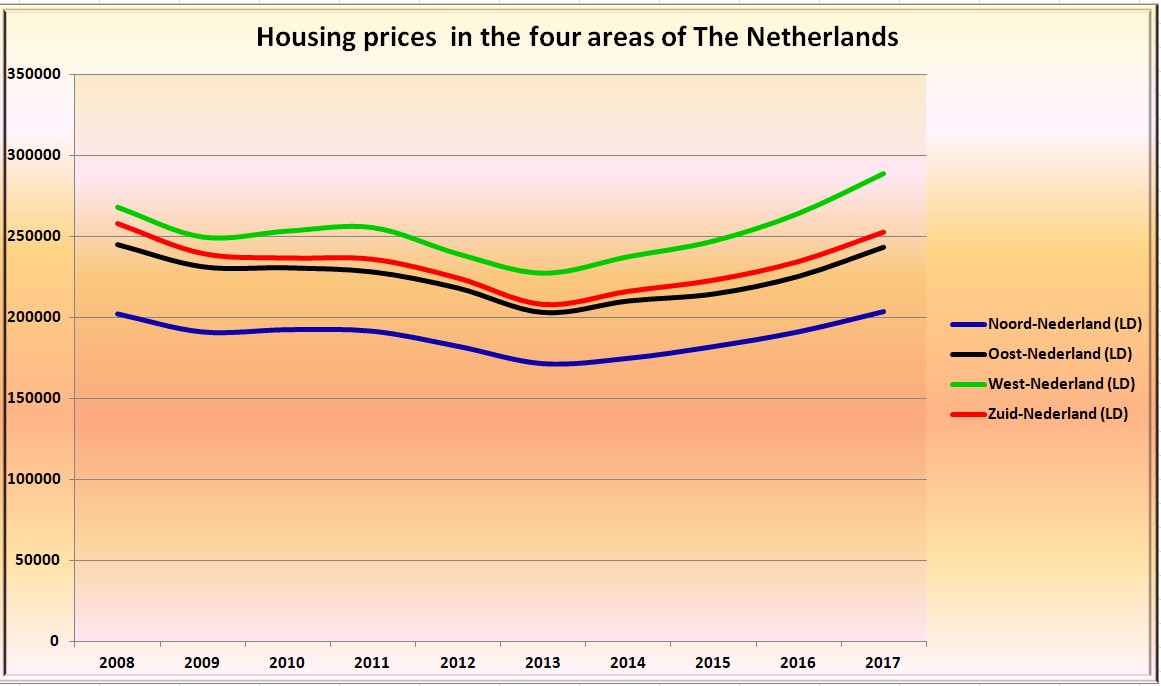

On

top of that, these extremely popular urban areas have almost certainly a

trickle down effect on the housing prices in neighbouring regions, even if

these are less popular among expats and/or Dutch middle class people. This

leads to the housing prices going up in general and all over the country, as

the following chart shows.

|

The average housing prices in the four areas of

The Nerherlands from 2010- 2018

Chart by: Ernst's Economy for You

Data courtesy of statline.cbs.nl

Click to enlarge |

Therefore

the current housing prices have equalled (and sometimes exceeded) the housing

prices since the crisis of 2007, when the housing crisis broke out.

Is that a healthy situation? No it is

not!

Can it continue? No, it cannot!

When the net wages of the Dutch

middle classes have actually dropped since 2008 (or since 2013 as a matter of

fact), but the housing prices have risen sturdily since then, a new and more

dangerous bubble has probably inflated.

And to make things worse: this bubble

must be close to popping!

The imploding housing bubble of 2007

did not have much to do with the American mortgage crisis, which was only

looming in those days. The real reason was that the housing prices in The

Netherlands were totally out of balance with the housing prices in countries

like Belgium and Germany, as they sat in 2007, and the people got fed up with

their ever higher mortgages.

The same situation is now also present

and perhaps even worse. I heard a radio interview with a Belgian realtor

shortly and his message was the same: Dutch people are more and more looking

for cheaper housing in Belgium.

What will be “the needle” to implode

this bubble?

I would say a sturdy increase of the

general interest rates, shaking out the pure speculators and cash strapped landlords,

who are over their heads in debt! But also an imminent buyer’s strike could

certainly be a possibilty, as the same happened in 2007 and led to a 30% price

drop.

All the signals are there that the

Dutch housing bubble might have a short life and that the explosion might send

shockwaves all over the country.

When the lower and middle classes don’t

have the money for Dutch housing anymore, the rise in housing prices cannot

last much longer!