Friday, 29 July 2011

Thursday, 28 July 2011

Air France-KLM suffers unexpectedly large loss in Q1 and blames it on increased fuel costs; I blame it on the lack of a healthy earnings model in the aviation business.

Only one month ago, Air France-KLM was in the news with a slick, marketing-driven story on the usage of cooking oil for fueling air planes.

Interested readers can read this again via my article: McDonalds proudly presents: the “McPlane”.

Today, however, Air France-KLM was bitten by reality, while presenting their Q1-figures for 2011-2012 (AF-K has a financial year not coinciding with the calender year).

The company has beaten the negative expections, by presenting a net loss of €197 mln for Q1, 2011. The Dutch financial newspaper Het Financieele Dagblad writes on this story. Here are the pertinent snips:

Aviation company Air France-KLM suffered an unexpectedly large loss, during the first quarter of book year 2011-2012. The French- Dutch company closed the quarter off with a net loss of €197 mln, according to the quarterly results, issued on Wednesday. That result was much lower than market expectation.

Air France-KLM states to have suffered from the strongly increased fuel prices. Those fuel prices soared by 16%, during this period that ended on June, 30th. Therefore the company’s kerosene bill increased by €232 mln.

Also the political unrest in Africa and the Middle-East and the nuclear disaster in Japan added to the aviation company’s bad results. These developments led to an additional loss of €100 mln.

The average analysts’ forecast stated that Air France-KLM would suffer a Q1-loss of €64 mln. In comparison: exactly one year ago, the aviation company enjoyed a net profit of €736, due to a one-off book profit of €1 bln.

The operational result was also negative: €145 mln. One year ago, that was €132 mln negative. Sales amounted to €6.22 bln: an increase of 9%, but almost €100 mln less than analysts expected.

The branch ‘Passenger-traffic ‘ saw sales increase by 10%, but was ultimately bearing a loss, with a gross revenue (ebit) of -/- €140 mln. Also ‘cargo’ was bearing a loss (-/- €14 mln against +€11 mln one year before), while sales slightly increased. The ‘maintenance’ branch, traditionally the most profitable area of the company, did add to the company’s result.

For calender year 2011, the company aims at a positive operating income.

The first thing that comes into my mind is: what were those well-rewarded analysts doing, when they missed the target for KLM by more than 200%.

The second thing is: when the company is bearing a substantial loss for Q1, bookyear 2011-2012 and the company had been bearing a loss of €264 (without the one-off book profit) for Q1, last year, there is ample reason for being worried.

And even more worrisome are the reasons for this loss, stated by Air France-KLM, that seemed to be ‘cut-and-pasted’ from the IATA’s Profit Outlook of June 2011 (see the link below in this article).

Yes, there have been unrest in the Middle-East and Africa. And yes, fuel became much more expensive. And yes, airlines are more vulnerable to shifts in fuel-prices, due to the excessive fuel consumption of airplanes. But one should remember, that fuel prices for airplanes are still without any taxes, in contrary to every other means of transport in the world, that must pay taxes on its fuel costs.

And Japan, the Middle-East and Africa were substantial problems, like the volcanoes were last year. But where these the kinds of problems that could bring a truly healthy company to its knees? Asking the question is answering it. And you might ask yourself: when will Air France-KLM write black figures again? And will it ever?

In my opinion, this is a very relevant question.

On June 6th, I wrote in my article, IATA blames profit drop for 2011 entirely on external circumstances:

And of course we had our share of setbacks in 2010 and 2011, thus lowering the profitability of the airliners: the ash cloud from the Icelandic volcano, the societal acrimony in North-Africa and Arabia, the earthquake and tsunami in Japan and the high oil prices that were the results of it. But hey, these are normal business risks and a healthy industry wouldn’t hardly notice those.

My opinion is that there is something structurally wrong within the aviation industry. When an industry has had a net return of 0.1% over the last forty years and when sustainable profitability for the aviation industry is still a mirage, like it is today, then you could seriously question the earnings model for the whole industry.

Especially when you consider that aircraft fuel – the main driver for aviation costs – is still free of taxes, due to an international agreement, where ALL other kinds of fuel for cars, trucks and other means of transport are (heavily) taxed by governments all over the world: gasoline, diesel/gasoil, LPG (Liquified Petroleum Gas) or fuel oil for ships.

You cannot see this loose from the development of passenger aviation over the last 20 years. Passenger aviation turned from a high-priced, high quality and high-service means of transport for the rich elite into a low-budget, mass transport medium that carries billions of people per year for bottom prices under – in some cases – poor circumstances.

The industry did this by slashing the ticket prices and stashing as many people as possible into an aircraft, while looking for maximization of the utilization rate of the airplane, by letting it fly almost around the clock. The relatively small group business class flyers pay – objectively looking – for the race to the bottom for economy class-passengers.

This race to the bottom was triggered by price-fighters like Easyjet and Ryanair in Europe, but was soon taken over by the established aviation companies. This is not a sustainable development, as in the end something's got to give.

And in May, I wrote in my article: Whatever the earnings model of Schiphol is, it surely ain’t flying:

What the figures make perfectly clear is that flying is almost considered an excuse for the existence of Schiphol. Although the figures of Schiphol Group are not totally clear about this, it is a well-known fact that aviation is in reality an unprofitable activity for Schiphol. But of course it is an indispensable condition for having an airport and due to tax-free kerosene and other tax-breaks, aviation can be executed at a very small loss. But the real money makers are consumers, participations and CRE.

In my opinion, the whole aviation and airport industry suffers currently from a fatally flawed and structurally unprofitable business model.

The industry is busy with an enduring battle for the cheapest tickets and an utilisation rate of airplanes that comes close to 99%, while on the other hand surprising the customers with all kinds of hidden charges and fees, up to (sometimes) 300% of the net ticket price.

This battle will last until the last airliner standing…. And I guess, it will only be a matter of time, until the first aviation company does fall over. And I wouldn’t even be surprised, if this leads to a domino effect of dropping companies in the whole aviation industry.

Seen in this light, Air France-KLM is not at all the worst operated airliner in the world. The company is big and strong and has especially favourable operating rights and a large network all over the world, compared to other airliners.

But the company needs to make serious money: not by asking hidden fees and extra charges from unknowing passengers, but by calculating a fair and square ticket price, without hidden tricks. A price that is sufficient for a net return of at least 10-15% of sales, instead of the 0.1% that seems to be the IATA standard.

However, before this will happen for Air France-KLM, some other airliners have to disappear first.

Wednesday, 27 July 2011

ING Bank ‘under suspicion’ of doing business with ‘rogue’ countries. Or how the US tries to put the whole world on their legal leash.

The Dutch financial newspaper ‘Het Financieele Dagblad’ writes a story on the Dutch multinational bank ´ING Bank´, being ‘under suspicion’ of doing business with the so-called ‘rogue countries’: Cuba, Iran, Syria.

For me this story was remarkable for two reasons. Here are the pertinent snips of this story, followed by my comments:

Public prosecution US investigates ING Bank

The American public prosecution started a criminal investigation against the Dutch, Amsterdam-based multinational bank ‘ING Bank NV’. The banks is under suspicion of violating sanction-regimes against Cuba, Iran and Syria.

A source close to Dutch national bank ‘De Nederlandsche Bank’ (DNB) expects that ING Bank might be penalized to the amount of ‘a few hundreds of millions of dollars’. The bank itself states that the investigation can lead to ‘substantial penalties or other sanctions’.

The exact content of these suspicions is not disclosed. The American authorities don’t react to requests for further information. ING doesn’t want to give detailed information during the investigation. The bank does state that the question is, if transactions in these three countries took place ‘according to the applicable rules’.

The American sanction regimes prohibit companies, that are active in the United States, to do business with countries that are enlisted as ‘rogue states’. The banks should especially be aware of dollar transactions with these countries. These transactions have to meet very strict demand.

As every international dollar transaction from everywhere in the world is settled through American banks, the US claim the right to worldwide prosecute banks that violate these rules.

ING Bank is already in the crosshairs of American law enforcement since 2006, according to annual reports of the bank. Until that year ING did business in Cuba, Iran and Syria without heavy restrictions. ING utilized the Netherlands Caribbean Bank, together with the Cuban government. But in 2006 the US became more restrictive. The Cuban ING branch came on amn American black list of businesses that were prohibited to do business with.

For me this news was remarkable for two reasons:

First: I worked from March 2008 until May 2011 at ING bank as an ICT consultant, with no connection to daily business at all. During that period, I took at least three mandatory courses on ING banking rules, in which it was specifically forbidden for all personnel to do business with Iran, Syria and Cuba in any way, whatsoever. So I hope and think that the bank has that subject covered, since 2006 .

Second: for me it is totally ridiculous, that the US claims the right to prosecute foreign banks for doing business outside the US, with these regimes.

If this business is executed by American branches of foreign banks on American home turf, American law enforcement are right to prosecute those branches. The US has, of course, the right to maintain their laws on their home ground.

But for me, it is a totally different story when a branch outside the US of a foreign bank does do business with Cuba, Iran and Syria.

To be clear:

· Iran and Syria are definitely rogue countries, but I can name a bunch that are also:

o Saudi-Arabia, Iraq, Afghanistan, Zimbabwe and Myanmar, to name a few. Are these regimes on that list? Or are these countries ‘too useful’ for the US?

· Cuba is definitely a dictatorship, but not at all the worst one. Cuba has just the bad luck, that the people that fled the country, after Batista was knocked over, are an influential group in Florida and other American states. And of course: the bad memories of The Bay of Pigs still play an important role.

· And what do you think: if Goldman Sachs would do business with Suriname or Myanmar and both countries would be under a sanction regime of the Dutch government, would GS pay €500 mln to the Dutch government? Really?!

I understand that the US is still the policeman of the world and the leading superpower and I do agree that this supplies the US with special privileges.

But:

· Whether a country is on the US sanction list, has a lot more to do with hypocrisy, opportunism and politics, than with justifiability, fairness and true compassion.

· It is just none of the US’ business, whether a European branch office of a European bank does do business with Cuba or not. The only situation where sanctions would be justified is, if a country is on a sanction list, composed and sanctioned by the UN Security Council. Not some unilateral list of ‘some’ country.

Tuesday, 26 July 2011

Latest figures from the CRE and RRE market show that the situation in The Netherlands remains… terrible.

New figures have been published on the markets for Commercial Real Estate (CRE) and Residential Real Estate (RRE). Both results were as surprising as the end buzzer in a basketball match: the figures were terrible.

Commercial Real Estate

The Dutch association for real estate agents NVM issued a press release on the Dutch market for office space. I show here the pertinent snips of this report, accompanied by my comments.

NVM Business: yet again more vacancy in market for office space (link in Dutch)

The Dutch market for office space is still quite negative. During the first six months of 2011, the supply of office space-for-rent increased by 4% to a record height of 7.03 mln sqr mt (75.67 mln sqr feet). Due to this increase in supply, 14.4% of all Dutch office space was for rent halfway this year.

Also at the demand side of the market, business was little inspiring, but a slightly increased transaction volume was a positive outlier. Although 505,000 sqr mt (5.43 mln sqr ft) was rented and sold, the realized volume was far from the normal level.

The increase in supply during the first half of 2011 was almost exclusively existing office space. In the newly built-segment only 10.000 sqr meter (107,000 sqr ft) was added. Although the increase in supply occurred at all regions of the country, the increase was most visible in the region South. This was caused by a expansion of the available square meters in cities like Breda, Den Bosch, Eindhoven and Maastricht. In the centres of these cities several buildings became available for the market. Also the middle of the country suffered from an increased supply.

Although the rental market for office space in region South was quite vivid, in the regions West-North and North the market suffered from a decrease in demand during the first six months. Rental and sales of office space in Amsterdam decreased yet again and in Groningen the demand for office space was virtually nil.

In spite of the further deterioration of the proportion between supply and demand on the Dutch office-market and the general drop of investments in CRE, the share of office space-investments in the average CRE portfolio remained fairly stable.

Investors invested a total amount of €420 mln in Dutch office space. Dutch investors had a share of €200 mln in investments. These were mainly private investors; institutionalized investors, like pension funds, insurance companies and CRE-funds stepped away from the office space-market and aimed mainly at shops and shopping centres.

I declared the Dutch CRE-market being in a coma at many occasions (for other articles, please use my search engine) and I have no reason whatsoever to change my tune. The aforementioned press release proves that I’m right.

The structural vacancy of office buildings is like a scar on the face of many cities and there is no reason to believe that this will change soon. The best thing that could happen is when structurally vacant office buildings are refurbished to student housing, social renting-houses or even condo’s for the free renting sector. This would meet the large demand for affordable rental housing in cities like Amsterdam, Rotterdam, The Hague and other cities with many students and office employees.

Residential Real Estate

Just like the market for CRE is still terrible, the RRE-market is still terrible too. The CBS issued its monthly report on the Dutch housing market:

Drop in house prices unchanged

Prices of existing owner-occupied houses were on average 1.9 % lower in June 2011 than in June 2010. According to the price index of existing residential property – a joint publication by Statistics Netherlands and the Land Registry Office – the price drop is about the same as in April and May.

All types of dwellings were cheaper in June 2011 than one year previously. Prices of flats dropped most (2.4 %). With 0.9 %, prices of detached houses fell the least.

Prices fell in all provinces. With 3.7 %, residential property prices declined most in Friesland. Prices in Groningen and Gelderland were 3.4 % down on one year previously. Prices of residential property in Zeeland remained almost stable (– 0.1 %).

Prices of existing residential property units dropped by 0.1 % compared with May 2011. The price drop was somewhat less substantial than in the two preceding months.

Around 9,500 existing owner-occupied houses changed hands in June, almost 13 % fewer than in June 2010. In the first half of 2011, nearly 58,000 houses were sold, a decline by 3 % compared with the same period in 2010.

Prices of existing own homes |

| The change of housing prices as a percentage Y-on-Y Source: http://www.cbs.nl/ |

At the beginning of this month, two third of the 6% conveyance duty on housing sales in The Netherlands was abolished. This triggered optimistic feelings among all people that were dependent from a free-flowing housing market:

· Real estate agents (represented by the aforementioned association NVM)

· The houseowner association Vereniging Eigen Huis.

· The Dutch banking and mortgage industry

· The government.

I gave my take on this government measure in the article: Dutch Finance Minister De Jager partially cuts conveyance duty….

The results on housing sales during July 2011 will be presented at the end of August. In advance, I doubt if these will be much better than the previous months.

The results for June were at least no surprise for me and will not be for my regular readers. You might want to check out the previously mentioned links here or you can use my search engine for further articles.

The good thing is that the mechanism of price destruction in the Dutch housing market is still in place. And price destruction is the only thing that can truly unlock the Dutch housing market. As bad news as this might seem for the current houseowners with their skyhigh mortgages, in the end it is the best solution for everybody.

Politics should worry about how to help mortgage-owners that are underwater, instead of keeping the housing prices artificially high. But that is a message that politics doesn’t want to hear.

Monday, 25 July 2011

International Card Services (ICS) in The Netherlands increases the interest rate on card debt from 15 to 16%: a serious reminder that credit card debt is not for free at all.

When my career as a financial ICT-consultant started in 1998, the first company I worked for was Visa Card Services (now International Card Services or ICS), at the time the sole issuer in The Netherlands for Visa credit cards.

I stayed there from 1998 until 2003 and had a wonderful time at this friendly, service-oriented and innovative company. Now it is eight years later and I still think with much pleasure of this company, that brought me financial knowledge, loads of working experience and job competence.

But today I was triggered by an article about what you could call the ‘dark side’ of ICS: the interest rate on credit card debt.

Today, ICS issued a press release that they increased the interest rate on credit card debt from 15% to 16%. This number, although it is not exceptionally high in comparison with other credit card issuers in Europe or the US, is in my opinion at the verge of loan sharking.

And it is quite easy to pay this kind of interest on your credit card debt. You don’t have to do much for this. In most cases, it is about what you don’t do as a customer: paying your bill in full.

To explain this: the worst kind of customer for ICS is a customer that doesn’t spend more than his credit card limit and pays his bill in full, once a month. At ICS in The Netherlands, a customer that pays his bill in full every month and stays within the limits, pays no charges at all on his credit card, except for the yearly subscription fee.

But if you ‘decide’ to pay back your credit card debt in installments, you do pay interest. And a lot of customers are initially not aware that they pay in installments.

This is how it works: a customer creates a credit card debt by shopping or by doing cash withdrawals and receives a monthly bill/statement for this.

If the customer can’t pay this debt back in full, because he forgets it or he just can’t do so at the time, his account is automatically changed to a 2.5% redemption account.

From that time on, he can keep on spending until he reaches his limit and he only has to pay back 2.5% of his credit card debt every month. And that is when the taximeter is running.

If a customer has a credit card debt of €3000 and he pays the total amount back in 40 installments at 16% annual interest, he pays a staggering amount of €3857.50 for a 3year4months loan.

But this is not what happens mostly: in practice, the customer probably keeps on using his credit card until he hits ‘his’ debt ceiling. And that is when the customer pays a whole lot more, especially when he decides to raise his debt ceiling.

At one time, the customer can get stuck with a credit card debt that he can’t afford to pay back anymore.

When you are already on a 2.5% redemption with your credit card and you want to prevent the former from happening, the solution is simple:

- pay your open credit card amount back in full.

- If you can’t afford to pay the amount back in full, try to get a personal loan or revolving credit at much lower interest rates (f.i. 7%) and repay your credit card debt with that.

- Don’t use your revolving credit as a new way to get into trouble

- Reinstate the 100% redemption on your credit card.

- And never spend more than you can afford from your monthly wages.

And if you are not sure that you can stop spending in time when you have a credit card, abolish the credit card and take a debit-card instead.

Germany: an economic miracle? Or the result of growing imbalances in Europe?!

As this article is a must-read in my opinion, but is printed in Dutch, here follows an integral translation of it:

Germany already sponges on foreign demand for a long, long time; just like China (by Marcel de Boer).

Analists like to use big words. When it concerns the economic growth in Germany Germany Germany Germany pull the rest of Europe up to a higher growth level’. For this reason the IMF advises Germany

Especially from the consumer’s side there is hardly an impulse for growth, at least not through his spendings. Retail sales is hardly moving upwards. To state it stronger: over the last months there has been a decrease in retail sales.

The restraint of the German Joe the Plummer, here called “Otto Normalverbraucher” (Otto Average-User) is not a new phenomena. He sits on his cash for years, already. That is no mystery; from the economic growth, he sees hardly anything back on his pay slip. An investigation executed by the economic institute DIW from Berlin, of which the results were published last week, showed that Germany employees LOST 2.5% in real income over the last ten years. The hardest hits were suffered at the bottom of the salary scales: some employees lost over 22% of real income.

German households were convinced to accept a smaller and smaller slice of the economic growth- pie, according to Michael Pettis of think tank Carnegie Endowment. For more than a decade these households subsidized German economic growth, with far-reaching consequences for the rest of Europe .

Around the new millennium, Germany chose a path of wage restraint, just like The Netherlands Portugal and Spain

Under the lead of the social-democrat German chancellor Gerhard Schröder, the consumer was made subordinate to the German trade and industry. Quickly, consumption lagged with production, according to Pettis. The surplus in goods and services was sold abroad, almost exclusively in Europe and especially in the part now called “the peripheral countries”: Portugal , Spain , Italy and Greece

Normally, it doesn’t take long before a country with a trade surplus sees its currency increase in value. However, as the Euro was deployed, this was not possible. Within the Euro-zone, Germany had an undervalued currency, while the countries that imported Germany

Implicitely, this was like a tax charge on German imports, according to Pettis. A charge, that acted like a subsidy for the German industry. In the peripheral countries, the industry was ‘taxed’ to subsidize imports. In a short matter of time, Germany could turn its lagging competitiveness into a lead: in 2000 Germany

As a consequence of the common currency, a situation evolved within the Euro-zone that could be compared with the relation between the US and Greece : as a consequence of underconsumption in China , together with the coupling of the yuan to the dollar, overconsumption evolved in the US

But the equasion goes further. China Germany (just like The Netherlands

Against these surplusses, there are equally large deficits on the capital account. Eventually, the external account must be balanced. An outflow of money from Germany

The peripherals should have used the cheap money to reinforce the structure of their economies. They received this advice from the ECB month after month, but ignored it. The money was mainly used for consumption and when it was invested, it was spent in the housing market, that was blown up to a bubble of massive proportions.

After five years, Germany China and Japan

But eventually the system stalls, as becomes clear in peripheral Europe and the United States Greece , Europe chooses for the last two possibilities. At the same time, people are aiming at an internal devaluation in the whole periphery. Through a decrease in wages and prices, the countries should become competitive again. However, when the Northern surplus countries are not willing to increase their consumption to a level above their production level, an deflatory hole originates and it will take a long time before European growth will be started again.

I was already aware of the dangers of the current imbalances within Europe , but this article explained it all in a wonderful, concise way.

And I’m convinced that Marcel de Boer is totally right in his conclusions on the German economy.

However, it will not be easy to increase consumption in Germany

I don’t want to advocate for enabling a price-wage spiral in Germany

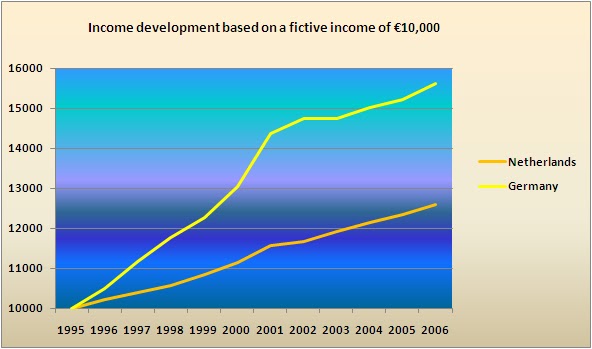

Although I don’t have the correct figures on the net income of German households, I’ve gathered some Eurostat statistics (ec.eurostat.eu) on the income development of German households, compared to Dutch households and put them in two graphs: the first graph shows the income development as a percentage of growth from 1996-2006 and the second graph shows the consequences of this income growth, based on a fictive annual salary of €10,000. I took Dutch data in comparison, as both countries are large net exporters and the people have a lot in common. Unfortunately, I don’t have more recent and detailed data available, but I think these graphs are still very telling:

|

| Income development as a percentage of growth in The Netherlands and Germany 1996-2006 source: ec.eurostat.eu |

|

| Income development in The Netherlands and Germany from 1996-2006, based on a fictive income of €10,000 (source: ec.eurostat.eu) |

These graphs show clearly the influence of a prolongued period of reduced income growth (Germany) on the spendable income, compared to a situation of ‘normal’, tendency-sensitive growth (The Netherlands). Based on a fictive start income of €10,000, reduced income growth resulted already in a difference in income of €3000 between Germany and The Netherlands. As the real incomes were probably higher, the difference will also be much bigger. This explains why the average German can’t spend so much, even if he had a desire to spend. This is especially true at the lower incomes, where the hardest hits were suffered.

Although the spending situation for consumers in The Netherlands in average is about the same as in Germany, the cause is different: the income growth, combined with the extremely low interest rates of the last 15 years, led to a spending spree in housing. Where a house in 1995 costed €100,000, the average price in 2007 was about 2.7 times higher: €270,000. This caused an extreme lock-up of money in housing and as a consequence reduced spending on (durable) consumption goods.

As a consequence of the locked-up Dutch housing market during the last four years and therefore the unability of Dutch houseowners to decrease their spendings on housing, the Dutch consumer is still very cautious about spending his income on consumption and durable goods. This effect is reinforced by the quite negative social mood and the credit crisis that resulted from this social mood.

Whatever the cause may be, the effect is that the cumulative imbalances between the northern and the southern European countries will not be balanced out, until consumption in The Netherlands, Germany and the other surplus countries is higher than production for a number of years. And that is bad news for whoever thought that the problems with the PIIGS-countries are over, since the last rescue attempt for Greece.

Subscribe to:

Comments (Atom)

Blogoria.de